Description

Fuyao was established in 1987 and is the #1 player in the global auto glass market with a mkt share of close to 35%. Fuyao has grown its market share from ~20% in 2013 on the back of building large competitive advantages via integration of supply chains and global manufacturing footprint. As a result, its customer base includes the largest auto OEMs both domestically and internationally; ~45% of its revenue base comes from outside of China (the firm is the key protagonist of Netflix documentary “American Factory”).

- AI Stock Screener

- how to invest in SpaceX

- how to invest in OpenAI

- warren buffett indicator

- current yield curve

Auto glass market has large barriers to entry, resulting in a pretty concentrated # of players – Fuyao is the largest followed by AGC and Nippon Sheet in Japan, Saint Gobain, and Xinyi. Auto glass manufacturers (i) require stringent safety and quality certifications at the local level as auto glass is one of the most fragile exterior facing part of a car during accidents; (ii) large local presence across sales and production bases as OEMs look for timely deliveries and (iii) most important of all, intensive capital investment required not only to set up the manufacturing facilities but also the production lines. As in many other industries, this is where Chinese manufacturing excellence and efficiency stand out. For example, a production line with capacity of 1mn sets of auto glass usually requires upfront investments of ~$70MM in the US vs. ~$30MM in China. Also production process is highly energy intensive – operating temperatures can reach close to 29,000 degrees F. Given all the above, only manufacturers with sufficient scale can meet all the requirements that also meet the demands of the large OEMs – thus resulting in a pretty concentrated industry.

Fuyao has topped competitors and has become the market leader in the global auto glass market due mainly through integration of supply chain and global distribution. One of the key advantages is that Fuyao is the only pure play auto glass player – as a result, it has maintained a higher R&D spending that most of its global peers who are more diversified and need to stretch their R&D budgets across various business lines. Another decision that has led to Fuyao gaining market share is that it has achieved self-sufficiency by integrating its supply chain all the way from sourcing upstream silica sand to float glass to molds and inspection fixtures. On the other end, Fuyao designs its won product lines with self-developed equipment, which brings down costs down by ~50% vs. purchasing from outside suppliers. Lastly, Fuyao started exporting glass since the 1990s, and is now fully integrated into the supply chain of all the mainstream OEMs (top 5 OEMs only make up ~15% of Fuyao’s top line). All of the above creates a flywheel effect as the fixed cost nature of glass production and Fuyao’s large scale advantages allows company to achieve higher operating efficiency through better allocation of resources over a diversified customer base across a global footprint. Large scale + increasing revenue base allows Fuyao to further re-invest into the business via capex and R&D thus taking market share and advancing technical expertise from competitors who have to reduce or cut capex/R&D investment as they continue to lose mkt share.

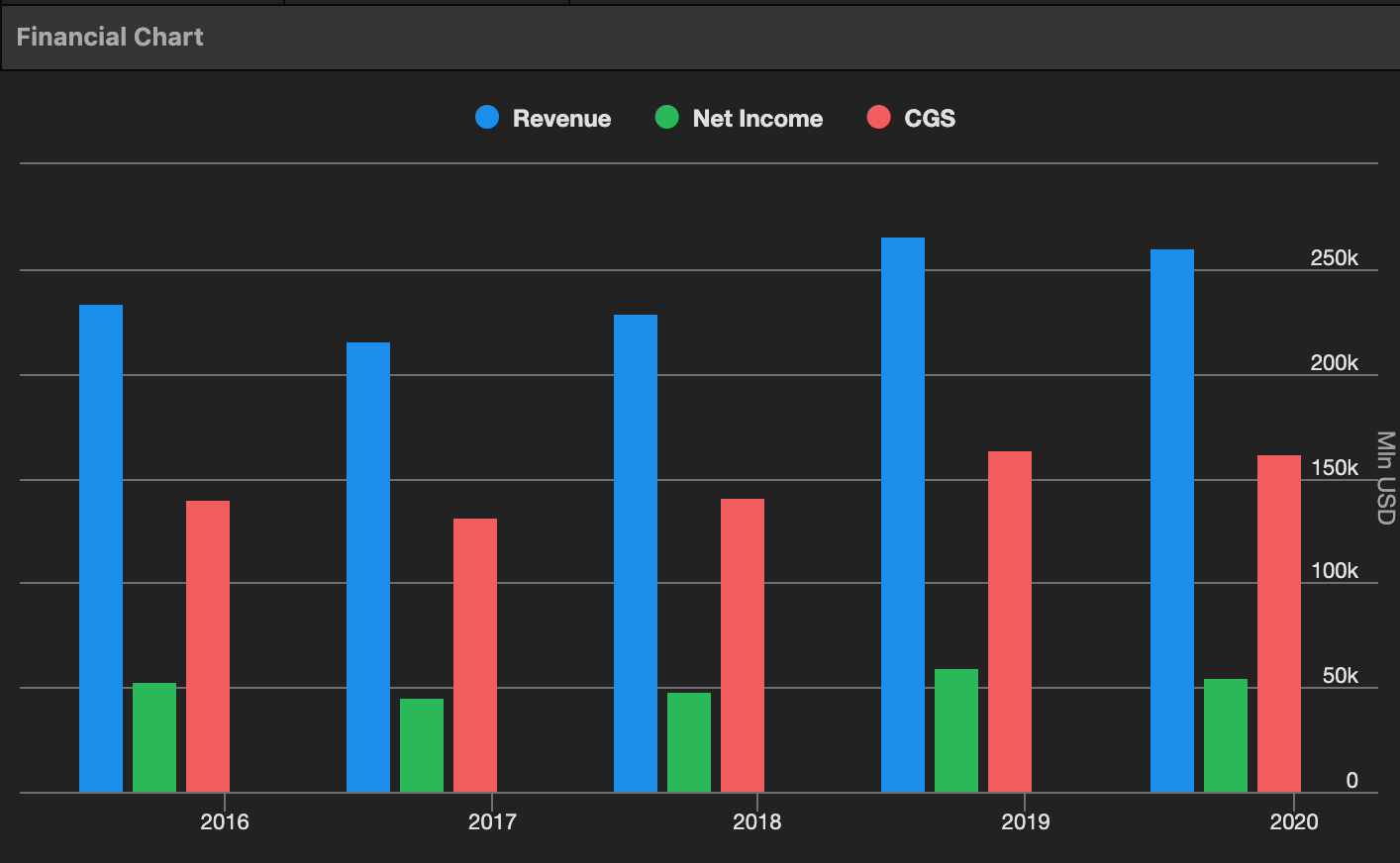

Fuyao has expanded its global market share from c.20% in 2013 to c.28% in 2021, on our estimates. With over 30 years' experience specializing in auto glass manufacturing, we think Fuyao has built a wide moat through its integration of supply chain, global reach, and most diverse customer base. A key example of its growing competitive advantage is a reporting from Bloomberg that Saint-Gobain is exploring a potential sale of its auto glass unit. This follows strategic decisions by Asahi Glass (AGC) and Nippon Sheet Glass to scale back and cut their auto glass capacities. Fuyao is the only player adding capacity while other scale back. Fuyao will add 13.5mn sets of auto glass capacity in 2025-26 (~31% of current capacity) vs. expanding ~5-18% of capacity every two years in the last round of capacity expansion in 2013-17.

Core the growth thesis for the name is an inflection in price as the mix shift of products will likely change materially driven by EV / autonomous driving (ADAS) adoption. This comes in two forms – all glass roofs and value-added glass functionality from ADAS. Tesla introduced an all-glass roof in 2016 on Model 3/ Model S and is set to become the standard across OEMs given the simplified structure and better integration of smart features. More importantly, OEMs prefer all glass roofs as the simplified structure results in cost savings of ~50%. Panoramic sunroofs entail more than a dozen components including glass panels, rails, sealing strips, and sunshades vs. just tempered glass under the closed-roof structure adopted by all-glass roof. More importantly for Fuyao, glass roofs have almost double the glass content resulting in prices roughly 2.5x that of traditional sunroof product it produces. All-glass roofs had almost negligible mkt share in 2020 and is expected to growth to > 40% next few years.

The second component of growth will be driven by a range of other value added products such as HUD (heads-up display) glass, tempered laminated glass, coated and heat-protecting glass, and glass with ADAS cameras. HUD is a display system that shows real-time driving information on the front windshield; it’s essentially an optical device with its technical barriers mainly existing in Picture Generation Unit (PGU), freeform optics and windshield glass. There have been three mass-produced types of products C-HUD, W-HUD, and AR-HUD, among which W-HUD and AR-HUD need windshield as the projection medium, which require wedge-shaped PVB in the glass or to coat the glass with a nano-film. Pricing costs range from $100 for C-HUD to $215 for W-HUD to > $400 for AR-HUD. W-HUD has been the most mainstream solution but newer models have been transitioning towards AR-HUD. AR-HUD penetration was at 0% in 2021 and expected to grow to 30% by 2030+.

A testament of the strategy in the works is the growth in the gross margins. Gross margins were at 33.2% 1Q23 and have grown to 38.8% by 3Q24 in an environment where we have seen global auto production slowdown. Fuyao’s revenue continues to grow by ~20% above the global auto production thanks to market share gains as well as ASP increases (+9% in 9M24 vs. mgmt guidance of 6-8%). High-valued added product mix increased 5.25% y/y to 58% in 9M24 - panoramic glass contributed ~9% of total auto glass revenue in 9M24. The proportion of revenue from HUD glass, tempered laminated glass, coated and heat-protecting glass, as well as glass with ADAS cameras was ~8%, ~7%, ~4%, and ~8% respectively in 9M24. In aggregate, these products have gone from 44% of sales in 2022 to now 58%.

Our expectation is that there is significant potential for the mix to grow to at least75% of the total revenue base driven significant pricing growth as the industry continues to transition towards EV and autonomous driving. Stock trades at consensus 15x ’25 P/E and 13x ’26 P/E despite generating top line growth of close to 20%